When Is 6% Versus 7% a Better Rate of Return???

When utilizing proper Gamma retirement planning strategies an investor can experience significant positive effect when taking income from their retirement portfolio. Most advisors today don’t employ a Gamma-Optimized strategy

“When it comes to generating retirement income, investors arguably spend most time and effort on selecting ‘good’ investment fund/managers – the so called Alpha decision – as well as the asset allocation, or Beta decision. However, Alpha and Beta are just two elements of a myriad of important financial planning decisions for the average investor, many of which can have a far more significant impact on retirement income.” -David Blanchette, CFA, CFP , Head of Retirement Research at Morningstar Investment Management and Paul Kaplan , Ph.D., CFA, director of research for Morningstar Canada

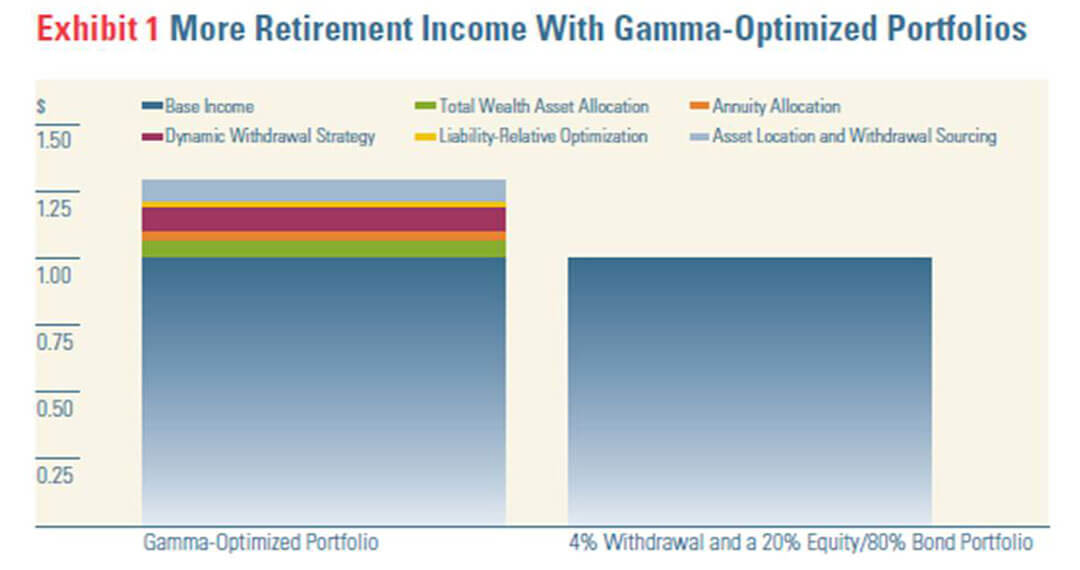

A research report written by David Blanchette, CFA, CFP, head of retirement research at Morningstar Investment Management and Paul Kaplan , Ph.D., CFA, director of research for Morningstar Canada entitled; Alpha, Beta, and Now …Gamma, explains that most retirees and their advisors are still focused on Alpha and Beta planning strategies which focus solely on investment management decisions when developing a retirement income plan. Both Alpha and Beta are statistical portfolio measurements. Alpha (negative or positive) measures manager effect within the portfolio, while Beta measures the risk or volatility of an investment portfolio versus a representative benchmark. Their research and paper concluded that utilizing a new statistical measurement they call Gamma (the effect that different retirement planning variables have on a retirement income plan) can now be confidently utilized for retirement income planning. As they explain, “We estimate a retiree can expect to generate 22.6% more in certainty equivalent income utilizing a Gamma-Efficient retirement income strategy when compared to our base scenario (traditional investment strategy only: Alpha/Beta planning). This addition in certainty-equivalent income has the same impact on expected utility as an annual arithmetic return increase of 1.59%”.

This is certainly an eye opening conclusion to an extremely thorough and riveting research report on Retirement Income Planning that absolutely validates why Your Retirement Advisor’s pragmatic and research based approach to retirement income planning works so well. The difference is that Your Retirement Advisor has looked at the research of Blanchette, Kaplan, Finke, Phau, and Milevsky, as well as many others over the years, and developed a pragmatic approach that incorporates many of the same principles and strategies for maximizing a retirees’ retirement outcome.

Volatility and Sequence of Return Risk Must Be Part of the Equation

As a quick reference, recent research has indicated that when a retiree begins to take income from their portfolio it’s imperative to reduce volatility in the portfolio in order to increase the portfolio’s survival rate. The evidence concludes that for any stated rate of return, the portfolio with the lowest volatility will survive the longest when taking income from the portfolio. On the converse, the portfolio with the highest volatility will suffer portfolio failure the quickest. With this knowledge, we constructed a portfolio to statistically reduce risk, to the greatest extent possible, while offering the highest return for that risk. Our recommendation was to utilize a moderate portfolio consisting of 50% diversified stocks and a 50% position in Equity Index Annuities (EIAs) linked to various globally diversified indexes.

In addition, a major risk that must be calculated to assess its effect on a retirement projection is Sequence of Return Risk. This is the risk that a portfolio will suffer major losses in the early years of retirement. This event would be known as “negative” Sequence of Return Risk and would have a negative effect on the survival rate of the portfolio (i.e. the portfolio would have a much shorter lifespan and a retiree would run out of money far sooner). On the converse, there is “positive” Sequence of Return Risk where the portfolio has tremendous upside growth in the early years or retirement. In a positive sequence of return environment a retirement portfolio would experience much greater potential portfolio survival (i.e. the portfolio would last much longer while taking income from the portfolio).

An “average” Sequence of Return Risk is a market environment where there is average or lower overall volatility in the portfolio which would give the portfolio moderate survival ability while taking income from the portfolio.

In summary, depending on the market environment (negative, positive or average) what the retiree experiences early in their income phase will have a direct effect on the portfolio survival rate…even with identical portfolio returns over the long term. A retirement income projection analysis must calculate the effect Sequence of Return Risk has on the long term survivability of a retirement portfolio. This will assure the highest probability of portfolio survival based upon the income strategy employed.

Based upon the below retirement projection, one can see how the practical application and effect of a Gamma-Efficient retirement income strategy can have greater impact on income when compared to a traditional Alpha Beta strategy that is employed by most retirees and advisors today. In this recently completed retirement projection for a new client we found the following:

After projecting the client’s traditional Alpha Beta retirement strategy (the “before” scenario), we reallocated the client’s current 80% diversified stock and 20% diversified bond portfolio to a more conservative allocation that would offer less return, but would dramatically reduce the portfolio’s volatility, while also offering reasonable growth potential. The client’s retirement projection variable was reset to the “new” reallocated portfolio and the results of the “before and after” are quite compelling.

The Results Speak for Themselves

The retirement projection assumptions utilized for this analysis were as follows:

Rate of Return Estimates –

Global Stock Portfolio @ 8% net

Global Bond Portfolio @ 3% net

Equity Index Annuity @ 4% net

Current Portfolio at 80% global stocks and 20% bonds = 7% melded return estimate (net)

Proposed Portfolio at 50% global stocks and 50% EIAs = 6% melded return estimate (net)

Additional Assumptions –

The client is currently 53 years old and preparing to retire at age 62 with a net retirement income need of $5,000 per month. We inflated her income needs at a 3% adjustment per year beginning immediately in the projection. Her current portfolio is valued at $450,107. She also has a small pension that will begin at age 65 paying her $11,124 annually. As well, the client will begin taking Social Security income at age 62 in the amount of $2,473 per month with a 2% cost of living pay increase per year. The client also has $25,000 per year rental income. We increased the rental property income at 1% cost of living adjustment. The analysis will also assume a marginal tax rate of 17%.

All these assumptions and variables were entered into our Retirement Income Projection Analysis (RIPA) system and here are the results:

The Results – Results presented on both a negative and average Sequence of Return environment

Negative Sequence:

Current Scenario – Age 90 Client Runs Out of Money

Proposed Scenario – Age 90 Client has $818,887

Average Sequence:

Current Scenario – Age 95 Client has $1,355,620

Proposed Scenario – Age 95 Client has $1,625,598

As we see by the above results, it’s imperative to develop a strategy that will utilize risk reducing investment vehicles to assure an income portfolio’s survival over the long term. Traditional stock and bond growth strategies employed by most are not enough. A Gamma-Efficient portfolio strategy must be utilized to assure the highest probability of portfolio survival.

Why 6% is better than 7%?

A new paradigm needs a new strategy: growth vs. income planning; Alpha Beta planning vs. Alpha Beta and Gamma strategies to generate a better retirement outcome.

As Blanchette & Kaplan explain, “Alpha and Beta are at the heart of traditional performance analysis; however, as we demonstrate, they are just one of the many important financial planning decisions, such as savings and withdrawal strategies, that can have a substantial impact on the retirement outcome for an investor.”

The above “current vs. proposed” is a very real and very typical scenario with many retirees. In most, if not all cases, the results will be the same… math is math and there’s really not much debate in how numbers calculate. This is an important and valuable outcome scenario where a combined stock and equity index annuity portfolio (generating a 6% return) is clearly better than a stock and bond portfolio (with a 7% return).

We have witnessed clients that are “annuity phobic” due to all the media’s misinformation and hype, as well as the all stock proponents who wrongfully claim that all annuities are too expensive. We’ve also witnessed clients that are “stock phobic” due to more rhetoric about how one can lose all their money in the stock market and stocks are no place for retirees to invest due to the risk. We purport that the best approach is a combination approach (based on research and factual numbers, not hearsay).

We also suggest several additional Gamma strategies/products to further increase the portfolio’s life expectancy:

Single Premium Immediate Annuities (SPIAs)

Dynamic Withdrawal vs. Traditional Static Withdrawal

Sound Social Security planning with sophisticated Social Security timing software

At Your Retirement Advisor we focus on the same five important financial planning decisions/techniques as suggested by Blanchette & Kaplan’s Alpha, Beta and now…Gamma research:

1) A total wealth framework to determine the optimal asset allocation

2) A dynamic withdrawal strategy

3) Guaranteed income products (i.e., annuities)

4) Tax efficient allocation decisions

5) Portfolio optimization that includes a proxy for the investor’s implicit and/or explicit liabilities

“We believe retirees deserve an investment and income planning experience that is founded on long-term, research and evidence-based results NOT rhetoric. And we’re committed to providing this for them.” -Your Retirement Advisor